Plan your taxes in 10 minutes!

Plan your taxes in 10 minutes!

We'll tell you how..

Yesterday, my brother spent 4 hours figuring out how to save tax for this financial year.

And he’s not alone. Most salaried folks need to submit their investment proofs to HR now, and we spend hours (and even days) figuring out how to save tax!

So today, I thought of summarizing everything in 5 minutes for you.

This newsletter is all you need to know to plan your taxes.

Okay let’s begin.

First, how is tax calculated?

Get your salary slip out and give it a good look at your gross income (without feeling sad about why the numbers are so low 😛)

First subtract all exemptions from your Gross Income

Then subtract all deductions

The amount you get is your taxable income

Now, check the slab it falls under, and calculate your tax liability

New or Old tax regime? Which one’s better for you?

First, let’s see the difference between old and new tax regime:

Now you ask, which one is better for you?

Unfortunately, there’s no straight answer! It depends on:

Your salary

What deductions you can claim

How many exemptions your company provides

Your eventual tax slab

You’ve got to compute your tax liability using both regimes and then decide which one is better for you!

Now here are the two elephants in the room - Exemptions and Deductions. In the next 2 minutes, you’ll understand exactly which exemptions and deductions are available for you to claim.

Exemptions

These are components of your salary on which you don’t need to pay any tax. They’re items which your employer will provide as part of your salary, so there’s not much you can do on your part to get more exemptions - it depends on your employer.

What you CAN do, is ask your employer to give you the relevant exemptions (although most larger companies won’t alter their salary structure for you - it’s a tough world out there).

Anyway, a brief of the major exemptions are given in the table below:

Next, comes the list of deductions that you can claim - now THIS is dependent on you - the more deductions you claim, the lower your tax liability will be.

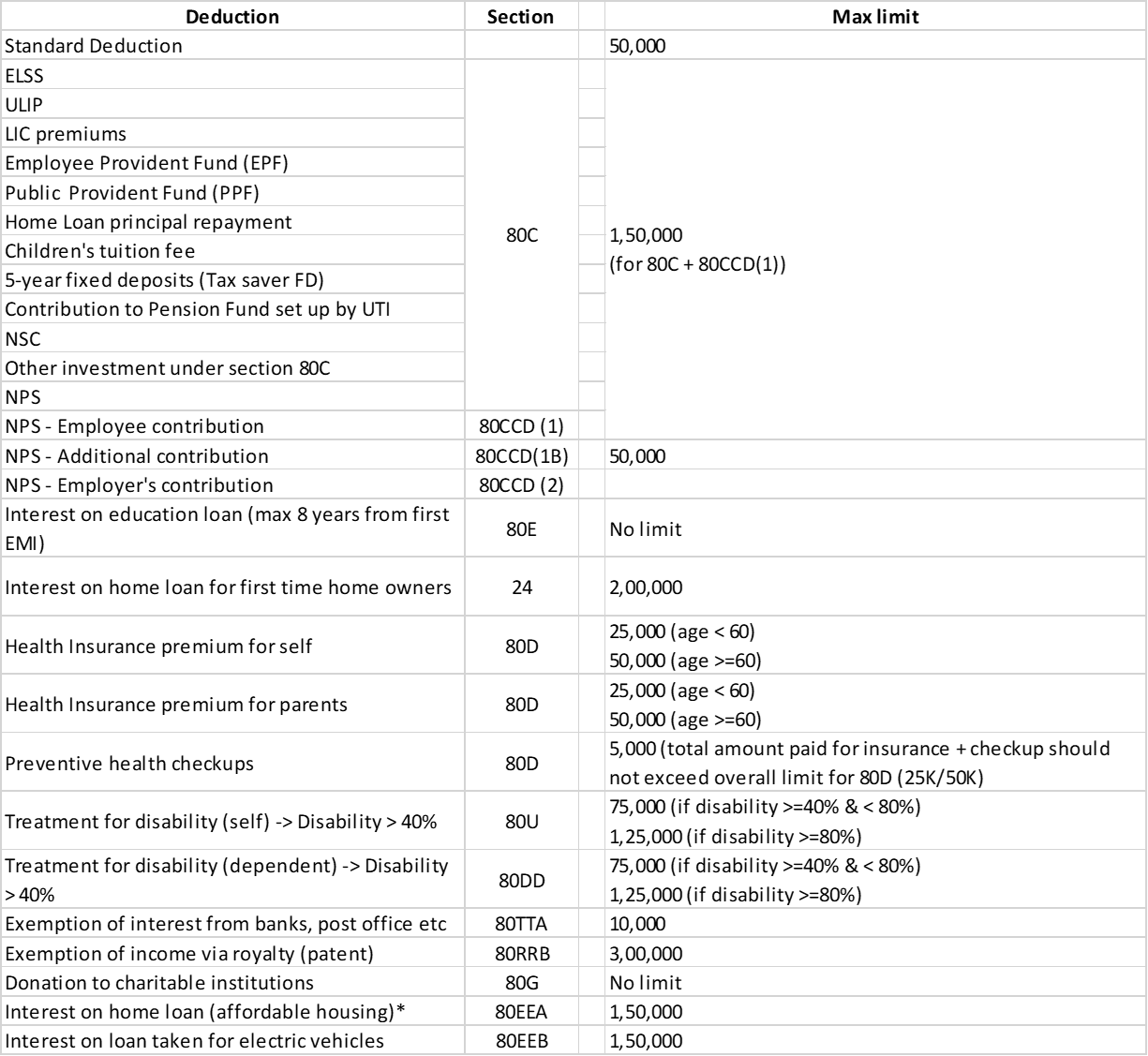

Deductions

Deductions are essentially expenses or incomes that you can claim - these expenses/incomes are not taxable.

Here’s a list of the major deductions you can claim, along with the limits for each.

* Section 80EEA has certain terms and conditions that you need to go through before claiming for it.

As a salaried employee, you can save tax only if you know the different exemptions deductions you can claim, and I’m hoping this article helped you understand them in detail, at one place.

Lastly, is there an easier way to calculate tax?

There is.

We have a few excel-based calculators where you simply input the data and you’ll get your tax liability without going through the hassle of calculating it manually. All of it won’t take more than 10 minutes!

All you need to do is share this newsletter on LinkedIn and/or Twitter and tag me (Ankur Jhaveri on LinkedIn, @jhaveriankur on Twitter) - We’ll send you the excel!

And if you have doubts, please feel free to comment on this article on Substack!

Have a lovely Sunday!

Hi Ankur. Thanks for this post. Very helpful. I’m working outside India and it’s been quite long since I last bothered about tax. Especially because I’m in Dubai where there’s no tax. Requesting you to make a post for people like me if you think I should still worry about tax because I may have some investments in India and income out of them. Just interested how to go about it.

Hey Ankush, last decade i used to file tax based on the Income but this year i am pursuing my Masters, do you suggest to file tax based on minimal income through interest, bonds maturity, FD maturities? Certainly 80G, 80D and NPS i am continuing despite non-employ category.